IPO and Equity Offerings

This book goes behind the scenes to examine the process of an offering from the decision to go public to the procedures of a subsequent equity offering.

For some public companies, the initial public offering is the one and only time they approach the equity markets. But for many newly listed companies, the IPO is the first transaction in a developing relationship with investors. Growth requirements mean that firms return to the equity markets either sporadically or regularly in the years following their initial listing. Another common reason for a follow-on offering, as secondary offerings are sometimes called, is when an existing shareholder wishes to raise more cash from its investment.

Fresh equity capital can be raised through a:

Marketed secondary offering

Rights issue

Bought deal

Accelerated bookbuilding.

Existing shareholders can reduce their positions through a:

Marketed secondary offering

Bought deal

Accelerated bookbuilding.

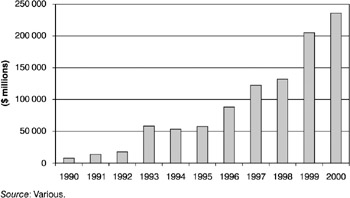

The volume of secondary offerings kept pace with IPOs in the 1990s, as illustrated in Figure 12.1.

A company whose share price has appreciated since its IPO will have an easier job of raising capital than a company whose share price is below its IPO price. Obviously, investors who have made money off a stock are more likely to be interested in purchasing more shares. Investors who missed out on the IPO may be more inclined to take a second chance to build a meaningful stake in a company.

We looked at the experience of Fairchild Semiconductor in Chapter 1. To recap, Fairchild raised $425 million in an IPO to fund its operations and pay down debt. Five months later, Fairchild returned to the markets, this time raising $903...