Real R&D Options

This is a practical guide to how organizations can use Real Option techniques to effectively value research and development by companies.

Applying It 's lemma to the value of the option, V( x,t), implies:

or

This means that the instantaneous rate of return on the option will be:

where:

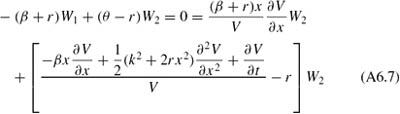

Now, suppose we invest W 1 in the underlying capital project, W 2 in options and W 3 in the risk-free asset, but in such a way that the investment is self-financing, or W 1 + W 2 + W 3 = 0. Then differentiation shows:

Substituting the stochastic differential equations for d x and d V into the right-hand side of this expression will then give:

Now, suppose we pursue an investment policy which eliminates all uncertainty, so that:

or

Since all uncertainty has been eliminated, arbitrage will dictate that the nonstochastic component of the investment policy will also have to be zero, or:

Simplifying the right-hand side of this equation gives:

which is the fundamental valuation equation contained in the text.

In the text we develop a pricing formula for a call option written on the net present value variable, with an exercise price of zero. Here, we solve the fundamental valuation equation under the more general boundary condition:

where E is a (non-trivial) exercise price. We again make the substitution V( x,t) = exp[ ? r( T ? t)] F( ?, ?), based on the co-ordinate system ![]() and ? = ( T ? t)/2. The fundamental valuation...

and ? = ( T ? t)/2. The fundamental valuation...