UK GAAP for Business and Practice

Complete with summaries of current standards and key implementation dates, this book provides a concise and easily accessible guide to all the recent changes in UK GAAP, and their likely practical impact.

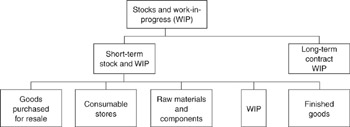

SSAP 9 (Stocks and long-term contracts) seeks:

to define practices of stock valuation;

to narrow the differences and variations as between different companies;

to ensure adequate disclosure in financial statements.

Aspects (2) and (3) are also covered by the Companies Act 1985.

SSAP 9 stock categories may be illustrated diagrammatically as follows:

Section 15.2 of this chapter is concerned principally with short-term stocks while section 15.3 deals with long-term contract work-in-progress.

The Companies Act 1985 balance sheet formats refer to:

raw materials and consumables;

work-in-progress;

finished goods and goods for resale;

but do not refer specifically to long-term WIP.

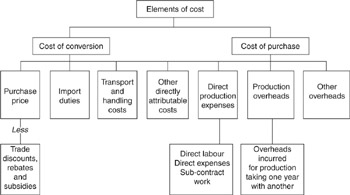

The basis of stock valuation under both SSAP 9 and the Companies Act 1985 is that individual stock items (or groups of similar items) should be valued for accounts purposes at the lower of cost and net realizable value.

The overriding principle is that costs to be included in the stock valuation should relate to expenditure which has been incurred in the normal course of business bringing the product or service to its present location and condition.

These costs will include both purchase costs and conversion costs. Relevant cost elements are illustrated below:

NRV is defined as actual or estimated selling price, net of any trade discount and after deducting any further costs expected to be incurred in completing,...