Linear Factor Models in Finance

Combining actual quantitative finance experience with analytical research, this book covers the science of asset pricing by concentrating on the most widely used modelling technique called linear factor modelling.

Three tests are implemented. The multivariate F test and the average F test are based on the linear regression framework: each of the n asset returns is specified as a linear function of the k factor returns. In the stochastic discount factor framework, the stochastic discount factor is assumed to be a linear function of the k factor returns and the parameters are estimated via the n moment conditions using the GMM with the weighting matrix advocated by Hansen and Jagannathan (1997).

Both the multivariate F test and the average F test start with the following multivariate linear regression:

| (6.12) | |

where ? i is a 1 k vector of factor loadings of asset i and f t is a k 1 vector of the k factor returns at time t. If the expected return of asset i is linear in betas, i.e. a linear combination of the k factors is on the efficient frontier, then

| (6.13) | |

Equation (6.12) and equation (6.13) imply that ?, the n 1 vector of n asset pricing errors, is jointly equal to zero.

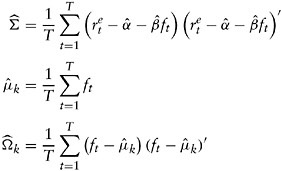

Assuming that the random error, ![]() , is normally distributed, together with assumptions stated in the first section, the multivariate F test is given by

, is normally distributed, together with assumptions stated in the first section, the multivariate F test is given by

| (6.14) | |

where

where ![]() is a vector of n 1 asset excess returns at time t, f t is a vector of

is a vector of n 1 asset excess returns at time t, f t is a vector of