Risk Analysis in Theory and Practice

Presenting a mix of conceptual analyses and applied problems, this book provides useful insights into the economic rationality of decision-making under uncertainty.

Chapter 4 presented an analysis of risk behavior under general risk preferences under the expected utility model. This provides some guidance for empirical risk analysis. However, applying this approach to decision-making under uncertainty requires having good information about two items: (1) the extent of risk exposure (as measured by the probability distribution of terminal wealth x), and (2) the risk preferences of the decision-maker (as represented by his/her utility function U( x)). Often, it is easier to obtain sample information about the probability distribution of x than about individual risk preferences. This raises the question, is it possible to conduct risk analysis without precise information about risk preferences? The answer is yes. This is the issue addressed in stochastic dominance. Stochastic dominance provides a framework to rank choices among alternative risky strategies when preferences are not precisely known (Whitmore and Findlay 1978). It seeks the elimination of inferior choices without strong a priori information about risk preferences.

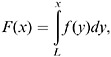

To present the arguments, consider a decision-maker with a risk preference function U( x), L ? x ? M, and facing a choice between two risky prospects represented by the probability functions f( x) and g( x). The associated distribution functions are

and

Under the expected utility model, f( x) ?* g( x) if and only if E f U( x) ? E g U( x), where E f and E g