A risk-adjusted performance (RAP) measure is a profitability measure that jointly takes into consideration the margin or profit produced by a business and its capital at risk (CaR). As noted in Chapter 6, we use CaR to refer to a one-year equivalent (if translation from subannual to annual data is necessary) of the VaR measures we discussed earlier in the book.

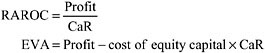

Perhaps the most well-known RAP measure is RAROC (risk-adjusted return on capital), which can generally be defined as the ratio between the profit and CaR for a given business area/unit. Another frequently used performance measure is Economic Value Added, EVA (originally developed by Stern Stewart and Co.), which is defined for banks as profit minus the cost of equity capital times capital at risk, i.e.,

Many banks use either of these measures or variants of these measures. While some have developed different acronyms, in most cases the underlying measures are only slight modifications either of the return-on-capital idea underlying the basic RAROC or of the concept of the value added over the cost of risk capital implied in EVA. In this chapter, we first clarify the two main reasons why a RAP measure may be calculated (Section 8.1). We then discuss the issues concerning the measure of profit and the difference between capital investment and allocation (Sections 8.2 and 8.3). The choice of the capital-at-risk measure to be used for RAP calculation is addressed in Sections 8.4 and 8.5. Section 8.6 critically compares RAROC and EVA measures.

Copyright Elsevier Inc. 2007 under license agreement with Books24x7